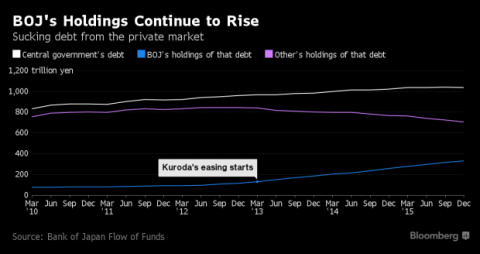

Last week, Bloomberg reported in depth on Japan’s miraculous diminishing debt load. Turns out, despite a steady rise in government borrowing, the burden of repayment is diminished because the buyer of 90 per cent of that debt is the Bank of Japan.

Last week, Bloomberg reported in depth on Japan’s miraculous diminishing debt load. Turns out, despite a steady rise in government borrowing, the burden of repayment is diminished because the buyer of 90 per cent of that debt is the Bank of Japan.

This has serious implications for Canadian investors, yet the full significance has not yet been thoroughly unpacked by media. My bet is most analysts and economists are aghast at this admission by a G7 government that debt could just be summarily forgiven. It suggests the notion of liability in credit does not apply to government, or its associated (yet private, to varying degree) central banks.

But it’s really quite simple.

The single most important rule upon which our global debt-driven economic growth equation is dependent is that debt is repaid. If it isn’t, assets are confiscated. Just like if you don’t keep up with the mortgage payments on your house, you lose it. But what happens when the biggest creditor is also the debtor? The entire debtor/creditor relationship is rendered nonsensical.

This post was published at David Stockmans Contra Corner on June 8, 2016.

Recent Comments